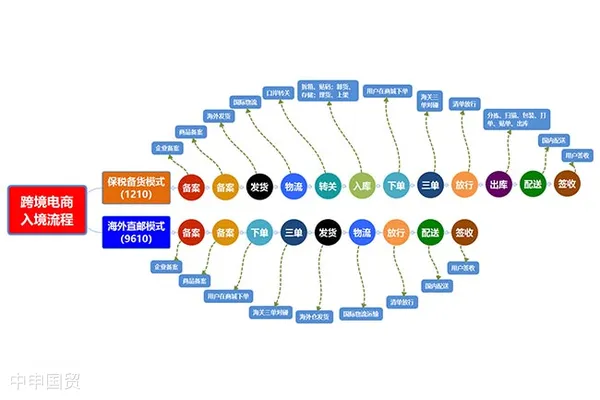

Scope of application for cross - border e - commerce retail imports

The tax policy for cross - border e - commerce retail imports is mainly applicable to two types of goods: First, goods traded through an e - commerce trading platform connected to the customs; Second, goods that enter the country through express delivery or postal enterprises without being connected to the customs. For the first type of goods, it must be possible to compare the electronic information of the three bills of the transaction, payment, and logistics. For the second type of goods, the express delivery or postal enterprise must provide unified electronic information and assume corresponding legal responsibilities.

These two types of goods must be within the scope of the List of Cross - border E - commerce Retail Import Goods. This scope of application ensures the compliance of imported goods and also imposes certain responsibilities and obligations on e - commerce platforms and logistics enterprises. Such classification helps the customs to manage imported goods from different sources and with different natures more effectively and precisely.

Current tax policies and tax calculation methods

The single - transaction limit for cross - border e - commerce retail import goods is 5,000 yuan, and the individual annual transaction limit is 26,000 yuan. Within these limits, the tariff rate of goods is temporarily set at 0%, and the value - added tax and consumption tax in the import link are levied at 70% of the legally payable tax amount.

To illustrate this more specifically, the article provides a practical example: A consumer purchased a 750 - ml bottle of imported French red wine through an e - commerce platform, with a total price of 1,000 yuan. Under the tax policy for cross - border e - commerce retail imports, the total value - added tax and consumption tax payable is 178.89 yuan. In contrast, if imported through general trade, the total tax will be as high as 431.34 yuan.

This difference shows that the tax policy for cross - border e - commerce retail imports reduces the tax burden on consumers to a certain extent, thus promoting the development of cross - border e - commerce.

Restrictions and other precautions

In addition to the above tax preferential policies, there are also some restrictions and regulations for cross - border e - commerce retail imports. First, if a single transaction exceeds 5,000 yuan or the individual annual transaction total exceeds 26,000 yuan, it will be taxed in full according to the general trade method. Second, the identity information of the purchaser (orderer) must be authenticated. This is to prevent illegal transactions and smuggling.

In addition, the purchased e - commerce imported goods can only be used for personal consumption by consumers and cannot enter the domestic market for resale. At the same time, if the consumer returns the goods within 30 days from the date of customs release, a tax refund can be applied for, and the individual annual transaction total will be adjusted accordingly.

These restrictions and regulations not only ensure the fairness and compliance of the tax policy but also prevent potential abuse and tax evasion. Therefore, both consumers and e - commerce platforms need to pay close attention to these regulations to avoid violating the law.

Tags: Tariff Foreign Trade Documents Cross-border E-commerce

Related Recommendations

? 2025. All Rights Reserved. 滬ICP備2023007705號(hào)-2  PSB Record: Shanghai No.31011502009912

PSB Record: Shanghai No.31011502009912